For years, the venture-capital playbook seemed remarkably straightforward: build software, scale quickly and benefit from attractive margins. In the age of artificial intelligence, that logic is beginning to change.

The reason is almost paradoxical. Software has never been easier to build. AI-assisted development tools allow founders to launch products faster, with smaller teams and significantly less engineering effort than before.

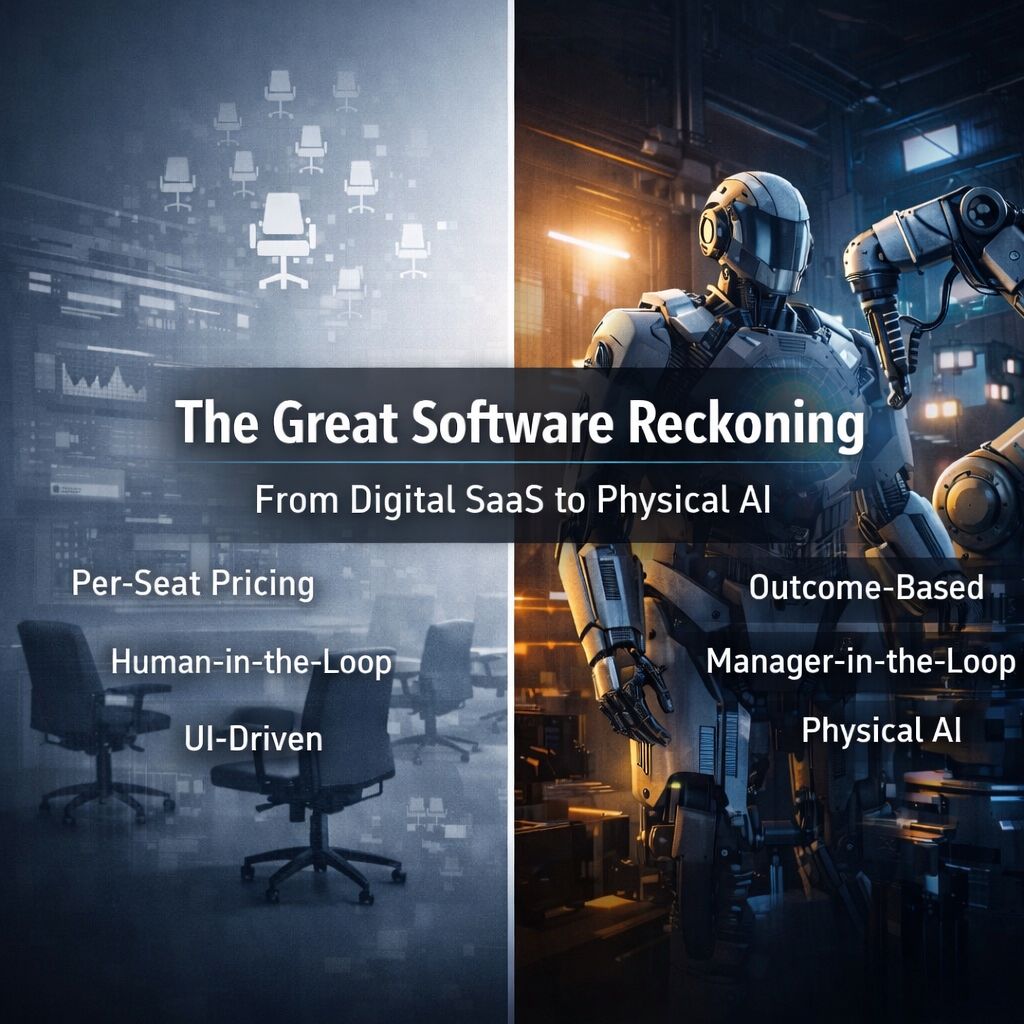

That is good news for entrepreneurs. But it also creates a new challenge: many software products are becoming easier to replicate. Features that once justified the creation of an entire startup can increasingly be reproduced within weeks, sometimes even days. As AI platforms improve, a simple software product is no longer necessarily a durable competitive advantage.

This is one reason why venture capital is moving back into the physical world.

The Rise of Physical AI

Investors are increasingly looking at areas that cannot be copied quite as easily: semiconductors, energy infrastructure, data centers, advanced manufacturing, robotics and so-called “physical AI.”

Physical AI describes intelligent machines that can understand their environment and perform complex tasks in the real world. This includes industrial robots, autonomous systems, drones and, in some cases, humanoid robots. The investment figures are striking.

According to PitchBook data cited by The Wall Street Journal, global venture-capital investment in robotics and physical AI increased from $4.2 billion in 2019 to $26 billion in 2025. By May 20, 2026, companies in these sectors had already raised more than $23 billion.

This is more than a short-term curiosity. It reflects a broader reassessment of where lasting value can be created in the AI economy.

Hype Meets Structural Change

As we recently discussed in our June Koyo newsletter, the shift from SaaS to physical AI contains elements of both hype and genuine structural change.

There is clearly a gold-rush mentality in parts of the market. Terms such as “physical AI,” “robotics” and “deep tech” attract attention quickly. Some robotics startups are reaching ambitious valuations long before their commercial potential has been fully demonstrated. But dismissing the entire movement as another AI bubble would miss the larger point.

Traditional software businesses were often built around speed: how quickly a company could develop a product, acquire customers and establish a strong position in a particular category.

AI changes that equation. Development costs are falling, product cycles are accelerating and many software features are becoming easier to reproduce. A basic software moat is often no longer enough. Hardware, industrial systems and advanced infrastructure are different.

Building a semiconductor company, an energy platform or a robotics business requires more than a strong product demo. It often requires specialized expertise, supply chains, production capabilities, regulatory knowledge and years of technical development. These constraints make such businesses harder to build but also harder to copy.

Is the Traditional Software Startup Dead?

No. But the bar is rising. The strongest software companies will continue to create enormous value. AI itself is primarily a software-driven transformation, and many of the most important companies of the coming decade will still be software businesses.

What is changing is the definition of a defensible software company.nLaunching a polished product is no longer enough. A credible moat may increasingly depend on proprietary data, deep workflow integration, a strong distribution advantage, network effects, brand, regulatory expertise or a unique position within a broader ecosystem.

The distinction is not simply between software and hardware. The more relevant distinction is between businesses that are easy to replicate and businesses that are difficult to replace.

A New Challenge for Venture Capital

The shift toward physical AI also creates a challenge for investors. Evaluating a SaaS startup is not the same as evaluating a robotics company, a factory, a chip architecture or a new industrial material. Investors need different expertise, different networks and a greater willingness to understand technical execution risk.

Not every venture-capital firm that succeeded in software will automatically succeed in deep tech. The next decade may therefore reward investors who combine the ambition of venture capital with a deeper understanding of industrial realities.

For founders, the message is equally clear: software remains powerful, but a thin layer of functionality is becoming increasingly fragile.

In the AI era, the most valuable companies may be those that connect intelligence with the real world or those software businesses that build a moat strong enough to survive in a market where building has never been easier.

Hinterlasse einen Kommentar